Buying your first home in Albuquerque is more achievable than a lot of people think, especially if you know what programs are available. New Mexico’s Mortgage Finance Authority (MFA) runs several assistance programs specifically designed to help first-time buyers cover the upfront costs that typically make homeownership feel out of reach. First-Time Home Buyer Programs in Albuquerque are available and make homeownership achievable.

This guide breaks down the programs currently available, who qualifies, and how to use them in the Albuquerque market.

What Counts as a First-Time Buyer in New Mexico?

You don’t have to be buying your first home to qualify. The MFA defines a first-time homebuyer as anyone who has not owned and occupied a primary residence in the past three years. That means if you previously owned a home but have been renting for the last few years, you may still qualify.

The MFA Programs Available to Albuquerque Buyers

The New Mexico Mortgage Finance Authority offers three core programs that work together. Most buyers use a combination of the first mortgage program and one of the down payment assistance options.

FirstHome: The Primary Mortgage Program

FirstHome is the MFA’s flagship first mortgage program. It offers a 30-year fixed-rate loan at below-market interest rates for eligible first-time buyers in New Mexico, including Albuquerque.

Key details for the Albuquerque area (Bernalillo County):

- Purchase price limit: Up to $481,176 for most New Mexico counties covers the majority of available inventory in Albuquerque

- Income limit (1–2 person household): Up to approximately $91,565

- Income limit (3+ person household): Up to approximately $105,300

- Minimum credit score: 620 (alternative credit qualification may be considered in some cases)

- Minimum borrower contribution: $500 from your own funds, which cannot be a gift or grant

- Homebuyer education: Required before closing; available online through MFA’s approved providers

- Occupancy requirement: Must be your primary residence within 60 days of closing

FirstHome can be paired with FHA, VA, USDA, or conventional loans, giving buyers flexibility depending on their situation.

FirstDown: Down Payment Assistance

FirstDown is a second mortgage loan that pairs directly with the FirstHome program to help cover your down payment and closing costs.

- Assistance amount: Up to $8,000

- Interest rate: 0% to no interest charges on this loan

- Monthly payments: None until you sell, refinance, or pay off the first mortgage

- Eligibility: Must be used alongside a FirstHome first mortgage

For most Albuquerque buyers, this is the most impactful piece of the MFA package. Pairing FirstHome and FirstDown means you can get into a home with significantly less cash upfront than a conventional loan requires.

HOMENow: For Lower-Income Buyers

HOMENow is a separate down payment and closing cost assistance program geared toward buyers at or below 80% of the area median income. It operates similarly to FirstDown but targets a different income bracket.

- Assistance amount: Up to $7,000

- Structure: Deferred second mortgage at 0% interest

- Forgivable: May be forgiven after 10 years if you continue to own and occupy the home

- Funding: Not always available, subject to funding cycles, so confirm availability with a participating lender

HOMENow and FirstDown are not used together; buyers qualify for one or the other based on income.

NextHome: For Repeat Buyers Too

If you don’t meet the first-time buyer definition but still have low to moderate income, the MFA’s NextHome program offers a similar combination of a fixed-rate first mortgage and down payment assistance. It’s worth asking a participating lender about this option if you’ve owned a home within the past three years.

Federal Loan Programs That Work Well in Albuquerque

MFA programs work alongside, not instead of, standard federal loan programs. The most common combinations Albuquerque buyers use:

- FHA Loans: Down payment as low as 3.5% with a 580+ credit score; 10% down with scores between 500–579. The most common pairing with MFA assistance for Albuquerque buyers

- VA Loans: Zero down payment for eligible veterans and active-duty service members; no mortgage insurance required. New Mexico has a significant military population. If you’ve served, this is the strongest option available

- USDA Loans: Zero down payment for buyers in eligible rural areas. Important caveat: Albuquerque city limits do not qualify as rural, so this program applies to surrounding areas like parts of the East Mountains, Rio Rancho, and smaller communities outside the metro

- Conventional 97: As low as 3% down for buyers with strong credit; no upfront mortgage insurance premium like FHA requires

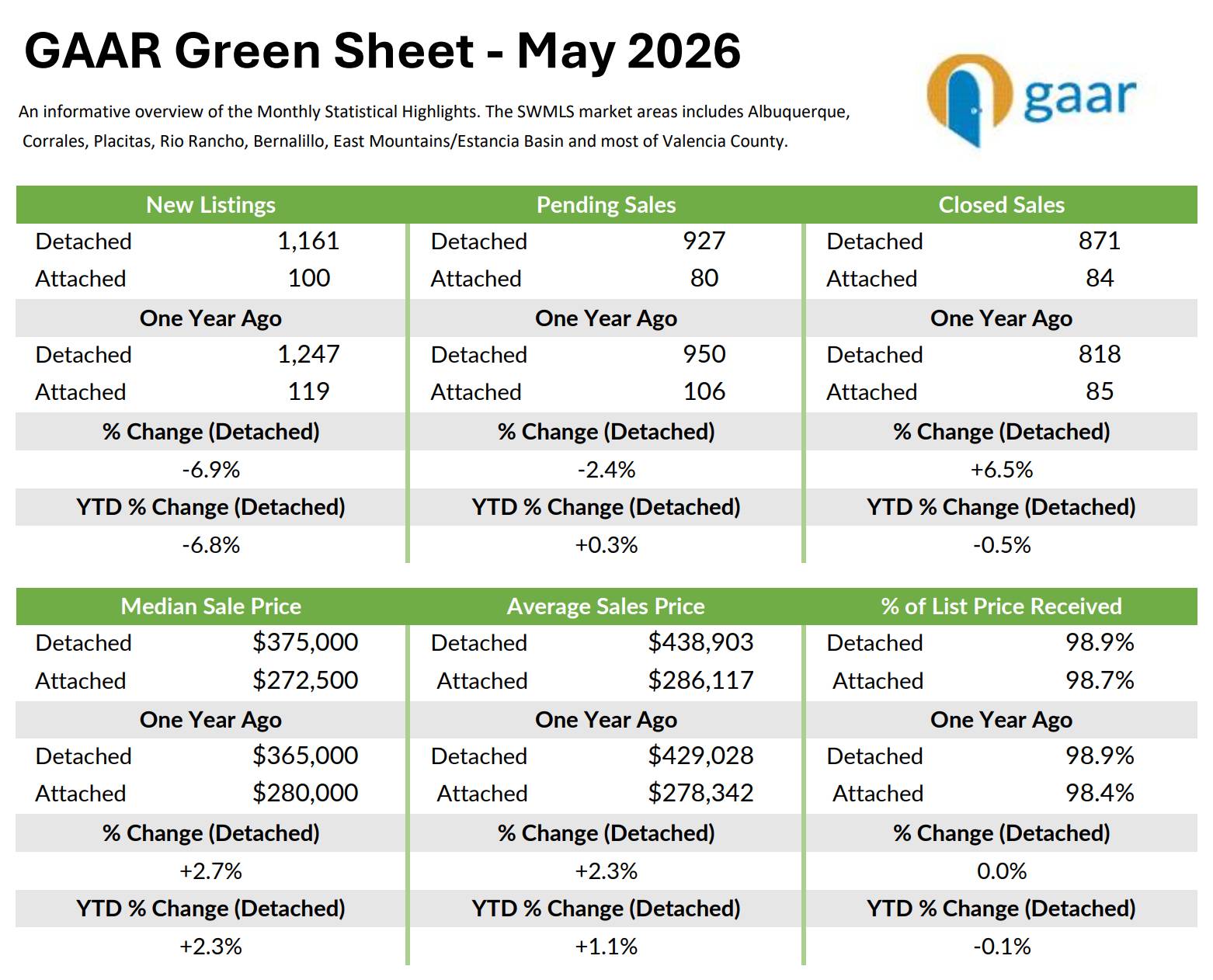

What Does It Actually Cost to Buy in Albuquerque Right Now?

Understanding programs is only part of the picture. Here’s what the numbers look like in the current market.

According to GAAR data, the median list price in Albuquerque was around $375,950 in late 2025, with the trailing twelve-month average sale price near $420,000. For a $375,000 home, here’s a rough look at what different down payment scenarios cost:

- 3% down (Conventional 97): $11,250 plus closing costs

- 3.5% down (FHA): $13,125 plus closing costs

- With FirstDown assistance: Up to $8,000 covered, meaningfully reducing your out-of-pocket at closing

- With HOMENow: Up to $7,000 covered, potentially forgivable after 10 years

Closing costs in Albuquerque typically run 2%–5% of the purchase price on top of the down payment. For a full breakdown of what to expect, see What Are Closing Costs in Albuquerque?

How to Actually Use These Programs

The process is straightforward once you know the steps. Here’s how it works:

Find a participating lender

MFA programs are only available through approved participating lenders in New Mexico. Not every bank or mortgage company offers them — you need to work with one that’s on the MFA’s approved list.

Complete homebuyer education

Required for all MFA programs. The MFA’s approved online course through eHome America takes a few hours and can be completed before you even start shopping.

Get pre-approved

Your lender will verify income, credit, and purchase price eligibility for the specific MFA program you’re applying for.

Shop within program limits

For most Albuquerque buyers, the $481,176 purchase price cap covers a wide range of available inventory, but it’s worth confirming the current limit with your lender before you fall in love with a property.

Close and move in

Occupancy within 60 days of closing is required for FirstHome. The home must be your primary residence, not an investment property.

A Few Things Worth Knowing Before You Apply

Program funding fluctuates.

HOMENow in particular is subject to funding availability. If you’re planning to use it, move quickly once you’re ready. Don’t assume it will be available indefinitely.

Income and purchase price limits update periodically.

The numbers in this post reflect current MFA guidelines as of mid-2026. Always confirm the latest limits directly with a participating lender or at housingnm.org.

USDA does not work inside Albuquerque city limits.

If you’re specifically buying within the city, FHA + MFA assistance is the most common path for buyers who need help with the down payment.

You still need $500 of your own money.

FirstHome requires a minimum $500 borrower contribution that cannot come from a gift or grant plan, for this regardless of how much assistance you receive.

Is This a Good Time to Buy in Albuquerque?

Albuquerque’s market has become more balanced heading into summer 2026. Inventory is still relatively tight.

GAAR data shows single-family home supply closed 2025 at 11,706 units, down 7% from the prior year, but days on market have stretched to around 60 days, giving buyers more time to make decisions than during the peak of 2021–2022. For a deeper look at current conditions, see Buying a House in Albuquerque This Summer: Worth It?

If you’re on the fence about timing, the programs above don’t care about interest rates; they reduce your upfront costs regardless of where rates are. And with Albuquerque home values up year-over-year, waiting typically means paying more. For the full market picture, see Albuquerque Housing Market: April 2026 Numbers Explained.

Ready to Use These Programs?

The first step is connecting with a participating MFA lender who can confirm your eligibility and walk you through which combination of programs makes the most sense for your situation. Every buyer’s income, credit, and timeline is different. A quick conversation with the right lender can tell you exactly what you qualify for.

Ready to take the next step? Contact us to get started!

Program details sourced from the New Mexico Mortgage Finance Authority (Housing New Mexico / housingnm.org) and GAAR 2025 market data. Income limits and purchase price caps are subject to change. Confirm current figures with a participating MFA lender before applying.